Borrowing base

[4] Borrowing base is frequently used for asset-based commercial loans offered by banks to corporations and small businesses.

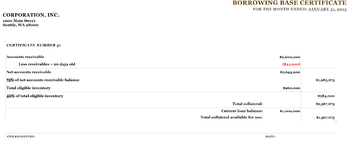

Typical industry standards are 75–85% for accounts receivable[1][12] and 25–60% for inventory,[7] and the advance rates can vary dramatically depending on the circumstances.

For example, Moody's is reportedly applying Monte-Carlo method over inventory price fluctuations within each industry to determine risk free advance rates.

[17] In case of revolving loans, lenders demand periodic recalculations of borrowing base and subsequently adjust the credit limit.

[23] Borrowing base of financial institutions who themselves apply for asset-based revolving loans is calculated by summing up all tangible working assets (typically cash, bonds, stocks, etc.)

In its paper form, a borrowing base certificate is signed by the authorized representative of the organization, typically by the organization's CFO, as errors in the calculation of borrowing base can result in various penalties (loan interest rate increase, demand of early loan repayment, etc.