Cheque

Cheques are a type of bill of exchange that were developed as a way to make payments without the need to carry large amounts of money.

Paper money evolved from promissory notes, another form of negotiable instrument similar to cheques in that they were originally a written order to pay the given amount to whoever had it in their possession (the "bearer").

[4][5] The newer spelling, cheque (from the French), is believed to have come into use around 1828, when the switch was made by James William Gilbart in his Practical Treatise on Banking.

[6] However, since the 19th century, in the Commonwealth and Ireland, the spelling cheque (from the French word chèque) has become standard for the financial instrument, while check is used only for other meanings, thus distinguishing the two definitions in writing.

[9][10] The cheque had its origins in the ancient banking system, in which bankers would issue orders at the request of their customers, to pay money to identified payees.

The use of bills of exchange facilitated trade by eliminating the need for merchants to carry large quantities of currency (for example, gold) to purchase goods and services.

In India, during the Maurya Empire (from 321 to 185 BC), a commercial instrument called the adesha was in use, which was an order on a banker desiring him to pay the money of the note to a third person.

[12][ISBN missing] Beginning in the third century AD, banks in Persian territory began to issue letters of credit.

[17][18] In the 13th century the bill of exchange was developed in Venice as a legal device to allow international trade without the need to carry large amounts of gold and silver.

Competition drove cashiers to offer additional services including paying money to any person bearing a written order from a depositor to do so.

Initially, they were called drawn notes, because they enabled a customer to draw on the funds that he or she had in the account with a bank and required immediate payment.

These were handwritten, and one of the earliest known still to be in existence was drawn on Messrs Morris and Clayton, scriveners and bankers based in the City of London, and dated 16 February 1659.

Birmingham, Bradford, Bristol, Hull, Leeds, Leicester, Liverpool, Manchester, Newcastle, Nottingham, Sheffield, and Southampton all had their own clearinghouses.

The documents are in some ways similar to modern-day cheques, with some data pre-printed on sheets of paper alongside blank spaces for where other information could be hand-written as needed.

In most western European countries, it was standard practice for businesses to publish their bank details on invoices, to facilitate the receipt of payments by giro.

A traveller's cheque is designed to allow the person signing it to make an unconditional payment to someone else as a result of paying the issuer for that privilege.

The use of credit or debit cards has begun to replace the traveller's cheque as the standard for vacation money due to their convenience and additional security for the retailer.

Most banks need to have the machine-readable information on the bottom of cheques read electronically, so only very limited dimensions can be allowed due to standardised equipment.

They are processed at the bank where they are presented, where an image of the cheque using Magnetic ink character recognition (MICR) is captured and digitally transmitted.

Electronic payment transfer continued to gain popularity in India and like other countries this caused a subsequent reduction in volumes of cheques issued each year.

It was possible to pay at the cash desk at the supermarket or shop by cheque or issue a check for annual school payments for a child.

Homeguard v Kiwi Packaging is often cited case law regarding the banking of cheques tendered as full settlement of disputed accounts.

As volumes started to fall, the challenges faced by the clearing banks were then of a different nature: how to benefit from technology improvements in a declining business environment.

In December 2009 the Payments Council announced its intention to phase out the use of cheques completely in the UK by October 2018, so long as adequate alternatives were developed.

[72] Most British utility companies charge lower prices to customers who pay by direct debit than for other payment methods.

Shell announced in September 2005 that it would no longer accept cheques at their UK petrol stations, a change replicated by other major fuel retailers.

[82] In the United States, cheques are referred to as checks and are governed by Article 3 of the Uniform Commercial Code, under the rubric of negotiable instruments.

[91][92][93] In the United Kingdom, in common with other items such as Direct Debits or standing orders, dishonoured cheques can be reported on a customer's credit file, although not individually and this does not happen universally amongst banks.

There a bank will pick up all the mail, sort it, open it, take the cheques and remittance advice out, process it all through electronic machinery, and post the funds to the proper accounts.

In modern systems, taking advantage of the Check 21 Act, as in the United States many cheques are transformed into electronic objects and the paper is destroyed.

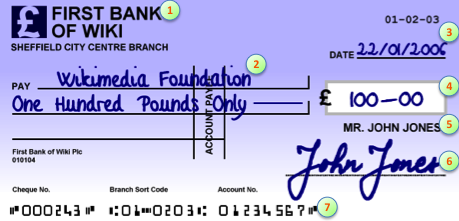

- Drawee

- Payee

- Date of issue

- Amount of currency

- Drawer

- Signature of drawer

- Machine-readable routing and account information