Volatility (finance)

[2] The generalized volatility σT for time horizon T in years is expressed as: Therefore, if the daily logarithmic returns of a stock have a standard deviation of σdaily and the time period of returns is P in trading days, the annualized volatility is so A common assumption is that P = 252 trading days in any given year.

of a year) is The formulas used above to convert returns or volatility measures from one time period to another assume a particular underlying model or process.

These formulas are accurate extrapolations of a random walk, or Wiener process, whose steps have finite variance.

However, more generally, for natural stochastic processes, the precise relationship between volatility measures for different time periods is more complicated.

This was discovered by Benoît Mandelbrot, who looked at cotton prices and found that they followed a Lévy alpha-stable distribution with α = 1.7.

When market makers infer the possibility of adverse selection, they adjust their trading ranges, which in turn increases the band of price oscillation.

[4] In September 2019, JPMorgan Chase determined the effect of US President Donald Trump's tweets, and called it the Volfefe index combining volatility and the covfefe meme.

These estimates assume a normal distribution; in reality stock price movements are found to be leptokurtotic (fat-tailed).

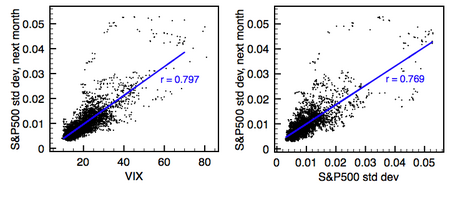

[6][link broken] It is common knowledge that many types of assets experience periods of high and low volatility.

[10] The risk parity weighted volatility of the three assets Gold, Treasury bonds and Nasdaq acting as proxy for the Marketportfolio[clarification needed] seems to have a low point at 4% after turning upwards for the 8th time since 1974 at this reading in the summer of 2014.

Breaking down volatility into two components is useful in order to accurately price how much an option is worth, especially when identifying what events may contribute to a swing.

The job of fundamental analysts at market makers and option trading boutique firms typically entails trying to assign numeric values to these numbers.

Using a simplification of the above formula it is possible to estimate annualized volatility based solely on approximate observations.

However importantly this does not capture (or in some cases may give excessive weight to) occasional large movements in market price which occur less frequently than once a year.

[18] In a similar note, Emanuel Derman expressed his disillusion with the enormous supply of empirical models unsupported by theory.