Real estate economics

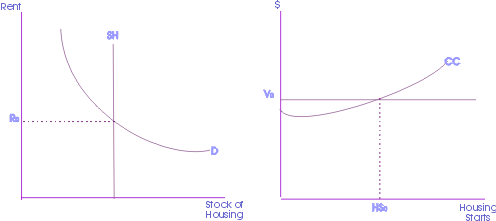

In order to apply simple supply and demand analysis to real estate markets, a number of modifications need to be made to standard microeconomic assumptions and procedures.

In acquiring mortgages on real estate, these institutions follow two main practices:[6] In addition, dealer service companies, which were originally used to obtain car loans for permanent lenders such as commercial banks, wanted to broaden their activity beyond their local area.

Despite legislation that could favor major banks, mortgage bankers and brokers keep the market competitive so the largest lenders must continue to compete on price and service.

[6] These cooperative financial institutions are organized by people who share a common bond—for example, employees of a company, labor union, or religious group.

The federally supported agencies referred to here do not include the so-called second-layer lenders who enter the scene after the mortgage is arranged between the lending institution and the individual home buyer.

A 2022 study published by three professors from the University of California found that people in the United States broadly misunderstand the role that supply plays in counteracting the price of housing.

As their property value increases, Conservative voters tend to consider, to a larger degree, houses, a form of self-supplied insurance, which disincentivizes support for such programs.

Those policy preferences are likely to be present to a greater extent when it comes to long-term social insurance and redistributive programs such as pensions due to the fixed nature of houses.

[15] (See below “The trade-off between Social policies and home ownership) Recently, several studies conducted in several European countries sought to determine the influence of housing on right-wing populist electoral results.

One explanation may lie in the fact that as the housing map created winners (those owning in dynamic areas) and losers (those holding in less prosperous areas), those who experienced a relative decline in the value of their homes tended to feel left out of a significant component of household wealth formation, and therefore were inclined to favorite populist political parties which challenged a status quo that did not benefit them.

Research in France shows that those who saw their home prices increase tended to vote for candidates other than Marine Le Pen in the 2017 French presidential election.

[16] In Nordic countries, studies tend to come to similar findings, with data showing an inverse relationship between house price increases and support for right-wing populist parties.

[12] Recent work by Julia Cagé and Thomas Piketty seems to corroborate the existence of areas’ prosperity determinants in the vote for right-wing populist parties.

[19] Such analysis, combined with previous presentations on house price variations, point in the direction that right-wing populist electoral results are, at least partly, driven by geosocial factors, with lower middle-class people living in less populated areas not feeling supported by traditional political parties and afraid of social downgrading.

As for the baby boomers, they tended to resent sympathy for the younger generations, recognizing that they were facing more significant barriers to home ownership.

Many government policies in social welfare states view houses as assets – a way for families to hedge their risks against eventual retirement and have a safe form of savings alternative to other pensions.

:[35] After the Great Recession, Ireland suffered from the Troika, resulting in Irish domestic laws undermining the social policies in favor of its financial health.

The Land and Conveyancing Law Reform Bill 2013 made it possible for lenders to repossess homes from borrowers - an action aimed at protecting the financial sector rather than having a coherent housing policy.

Denmark used a mortgage-based covered bond system as its form of “privatized monetary policy,” in 1986, the housing bubble burst, leading to the coalition government reducing the mortgage interest deductibility from taxes.

When the housing bubble burst in 2008, the socialist Gordon Bajnai administration (2009-2010) focused on reducing public debt and deficit rather than the private side (over-indebted population).

The academic debate around the causes for rising levels of mortgage debts concerns their focus on the supply or the demand side of the housing market.

Schwartz states that the 1980s deregulation of mortgage markets increased potential credit, resulting in higher demand for real estate and rising prices.

[39] In addition, Johnston and Regan showed that increased wages led to households having more liquidity to finance real estate properties, leading to higher demand for houses and, therefore, even more mortgage lending.

[40] This side of the academic debate presents an argument that seeks to use increased demand for housing over the years as the primary reason for rising levels of mortgage debt worldwide.

[41] In summary, the study presented that the three countries rode the waves of political policies that were formed around the right/center-right governments’ desire in the 1990s to stimulate home ownership and reduce social housing expenses and build a society of self-sufficient home-owners.

Danish banks saw their annual growth rates in lending exceeding 50% between 2003 and 2007, while in the Netherlands, the Dutch market for securitized assets (in this case, mortgage-backed securities) became the second largest in Europe after the UK in 2008.

[43] In summary, the scholars argue that the Netherlands, Denmark, and Sweden mortgage markets were liberalized to encourage financial innovation and promote homeownership.

About twenty years later, Frank Castles, a professor of political science at the Australian National University, conducted more in-depth research on Kemeney’s thesis and strongly confirmed his case.

I argued that an overwhelming emphasis on home ownership created a lifestyle based on detached housing, privatised urban transport and its resulting ‘‘one-household’’ (and increasingly ‘‘one-person’’) car ownership, a traditional gendered division of labour based on female housewifery and the fulltime working male, and strong resistance to public expenditure that necessitated the high taxes needed to fund quality universal welfare provision.” [46]In 2020, Gunten and Kohl returned to Kemeny’s thesis.

In conclusion, Gunten and Kohl present a case where the inverse relationship between homeownership and social policies existed in the 80s but has changed towards the dual ratchet effect of simultaneous, upward convergence.