John Whitmore (accountant)

John Whitmore (c. 1870 - March 18, 1937[1]) was an American accountant, lecturer, and disciple of Alexander Hamilton Church, known for presenting "the first detailed description of a standard cost system.

"[2][7] In his 1906 article "Factory accounting as applied to machine shops," Whitmore "elaborated upon and explained in considerable detail the costing system advanced by A. Hamilton Church, adopted the manufacturing account (work in process) arrangement for controlling the factory cost sheets"[8] in machine shops.

"[9] Emile Garcke, and John Manger Fells (1912/1922) explained the most regular system of dealing with machine rates in those days.

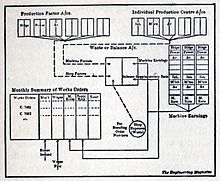

The further suggestion has therefore been made that the balance remaining on each plant account, being the difference between the amounts charged off on the before mentioned assumption, and the actual lessened value should be charged off by means of a supplementary rate to an Idle Capacity account, as representing a loss, or more correctly, a non-realised gain, consequent upon the non-utilisation of the plant to its full capacity.

The information thus obtained would be of great value to the manufacturer in considering how he can, having regard to market and other conditions, realise from his plant the maximum economic advantage.

The importance of this consideration cannot be too strongly emphasised, for whilst in the case of labour the number of employees directly engaged in production can be regulated from time to time by the volume of trade, such readjustment is not possible in the case of machines whose maintenance, standing charges, and depreciation have to be provided for, whether idle or employed.

If the results of the additional rates are charged off to the Stock or other orders, without being specially noted, it would seem that so good a measure of the idle capacity of the plant would not be obtained as by the procedure before described.

3, Journal of Accountancy, 106, says:"At scarcely any point are the figures absolutely final, free from all qualification and all contingencies, but the latter are recognizable, and, generally speaking, arise from the uncertainties that are a condition of the work done.

"The objection to the application of the system to railroad accounts are enumerated with great force by Prof. Logan G. McPherson in his book, "The Working of the Railroads,"...[13]In 1915 Whitmore gave lectures series of lectures at Harvard University with the following topics:[5] In 1918 Whitmore and Henry Gantt were expert witnesses in a lawsuit about newsprint manufacturing conditions and price-fixing.

(1968) Michael Chatfield already cited another source, that credited Whitmore as being "the first detailed description of a standard cost system.