Consumer debt

Debt also leads to a lower credit score and may have effects on mental health.

On a monthly basis, this debt ratio is advised to be no more than 20 percent of an individual's take-home pay.

[2] The interest rate charged depends on a range of factors, including the economic climate, perceived ability of the customer to repay, competitive pressures from other lenders, and the inherent structure and security of the credit product.

The permanent income hypothesis suggests that consumers take debt to smooth consumption throughout their lives, borrowing to finance expenditures (particularly housing and schooling) earlier in their lives and paying down debt during higher-earning periods.

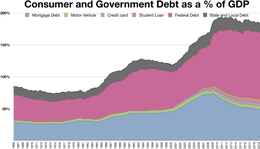

According to the US Federal Reserve's 2024 statistics, the US household debt service ratio was at its lowest level since its peak in the Fall of 2007 in 2021, but has since risen.