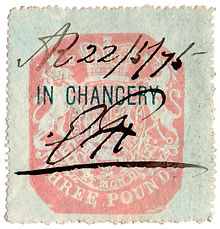

Stamp duty in the United Kingdom

During the 18th and early 19th centuries, stamp duties were extended to cover newspapers, pamphlets, lottery tickets, apprentices' indentures, advertisements, playing cards, dice, hats, gloves, patent medicines, perfumes, insurance policies, gold and silver plate, hair powder and armorial bearings.

[5] The attempted enforcement of the Stamp Act 1765 in the British colonies in America led to the outcry of "no taxation without representation".

In 1808 stamp duty on conveyances of sale, including transfers of land and shares, became an ad valorem tax.

Apart from transfers of shares and securities, the issue of bearer instruments and certain transactions involving partnerships, stamp duty was largely abolished in the UK from 1 December 2003.

[10] Aside from an exemption for 'qualifying intermediaries' such as market makers at large banks,[11] Stamp duty reserve tax (SDRT) was introduced under the Finance Act 1986 to ensure that a form of tax equivalent to stamp duty would continue to be payable on the transfer of uncertificated shares.

[12] A higher rate of SDRT at 1.5% is charged for the issue or transfer of shares to a person who operates a depositary receipt scheme or a clearance service (other than CREST, which is exempted).

The higher charge compensates for the fact that later transfers of depositary interests or through the clearance services will not attract SDRT.

This type of SDRT is by nature paid almost exclusively by offshore (i.e. non-UK) investors, primarily US fund managers and amounts to approx.

Over several years after its July 2000 acquisition of CCF, HSBC and its custodians mounted lawsuits[13] against HMRC alleging that the levying of the 1.5% SDRT charge on delivery of HSBC shares into Euroclear as consideration for the acquisition of CCF shares breached EEC Directive 69/335/EEC on capital taxes.

SDLT is not a stamp duty, but a form of self-assessed transfer tax charged on "land transactions".

[17][18] For typical transactions in land, such as the buying and selling of a residential house, there is little change from stamp duty, except that a tax return is required to be made to the HM Revenue and Customs (previously Inland Revenue) and documents no longer need be given a physical stamp.

The removal of the "slab" structure in 2014 meant that all purchases under the threshold were tax free, regardless of the status of the buyer.

[23] In the 2010 budget, the chancellor ended stamp duty on homes under £250,000 for first-time buyers for a two-year period, while introducing a new 5% rate for properties over £1,000,000.

In the budget of 2012, Chancellor George Osborne introduced a new 7% level for properties over £2,000,000 to assuage Liberal Democrat demands for a mansion tax.

[35] The changes made in the 2014 Autumn Statement caused a collapse in the number of sales of more expensive properties.

[36][37][needs update] In October 2015 the Spatial Economics Research Centre produced a report detailing the distorting effects of stamp duty on the housing market.

[38] In years prior to 2005, there had been a high level of house price inflation in the UK but no change in these thresholds, leading to a substantial increase in the revenue from SDLT through bracket creep.

[41] For residential house purchases, the current rates in England & Northern Ireland from 23 September 2022 are as follows:[42] As part of the response to the COVID-19 pandemic, the 2020 Summer Statement introduced a temporary reduction in stamp duty for buyers in England and Northern Ireland completing purchases before 31 March 2021 with no stamp duty due on the first £500,000 of property value.

[45] Prior to 4 December 2014 the rates were as follows:[46] At this time, SDLT worked on a "slab" basis, so the above percentages apply to the whole of the purchase price.

[47] For example if the residential property your are purchasing is uninhabitable (for example: severe leakage, mould, asbestos or unsafe wiring) then tax relief or an exemption may be obtained.