Taxation in Spain

Taxes in Spain are levied by national (central), regional and local governments.

Four historical territories or foral provinces (Araba/Álava, Bizkaia, Gipuzkoa and Navarre) collect all national and regional taxes themselves and subsequently transfer the portion due to the central Government after two negotiations called Concierto (in which the first three territories, that conform the Basque Autonomous Community, agree their defense jointly) and the Convenio (in which the territory and Community of Navarre defense itself alone).

As in other jurisdictions income tax is payable by both residents and non-residents with different rates applying.

Sporadic periods of time outside of Spain are not counted towards establishing oneself as a non-resident for tax purposes.

Also, the amount may be reduced by declaring income with your spouse if you are married and some expenditures (like contributions to unions, personal pension funds, etc.).

There are also other reductions and deductions applicable for expenditures and housing (home rental and purchasing).

Some autonomous communities (like Cantabria, Castilla-La Mancha and Madrid) have different allowances for their own share of the income tax and also establish their own deductions.

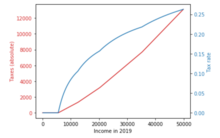

Once the gross income has been reduced by the legal allowances, reductions, and deductions, the taxpayer has to apply the rate to find out the actual tax.

The communities of Andalusia and Catalonia apply a higher regional income tax than Madrid.

VAT (IVA in Spanish: impuesto sobre el valor añadido or impuesto sobre el valor agregado) is due on any supply of goods or services sold in Spain.

The 10% rate is payable on most drinks, hotel services, and cultural events.

Second-hand properties are not subject to VAT, but a transfer tax, known as Impuestos Sobre Transmisiones Patrimoniales or ITP.

The rate, which was introduced in 2015, is set at 15% for the first 2 years in which the company obtains taxable profit.

Property owners are considered a non-resident in Spain if they live in the country for less than 183 days in a single year.

Non-resident property owners are required to make a tax declaration for each quarter in which they have earned rental income.

“Impuesto Sobre la Renta de no Residentes” is a tax on rental income for non-resident landlords in Spain.

Where a property has only been let for part of a year, Spanish Deemed tax is applicable only for the period in which it was vacant or occupied by the owner for personal use.

Any income exceeding that maximum base is not subject to both employee and employer contributions.