Management control system

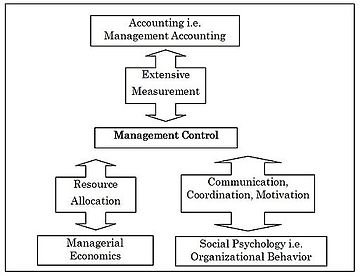

[4] According to Maciariello et al. (1994), management control is concerned with coordination, resource allocation, motivation, and performance measurement.

Consequently, a management control system should include a comprehensive set of performance aspects consisting of both financial and non-financial metrics.

Therefore, depending on the balance between financial and non-financial measures, a management control system may be characterized as finance-oriented or operations-oriented.

Finance-oriented control systems are primarily based on financial accounting data, such as costs, earnings or profitability, whereas operations-oriented control systems are primarily based on non-financial data that focus on operational output and quality, for example service volume, employee turnover, or customer complaints.

[citation needed] According to Horngren et al. (2005), management control system is an integrated technique for collecting and using information to motivate employee behavior and to evaluate performance.