Microfinance

Microfinance includes microcredit, the provision of small loans to poor clients; savings and checking accounts; microinsurance; and payment systems, among other services.

[8] The history of microfinancing can be traced back as far as the middle of the 1800s, when the theorist Lysander Spooner was writing about the benefits of small credits to entrepreneurs and farmers as a way of getting the people out of poverty.

[citation needed] Independently of Spooner, Friedrich Wilhelm Raiffeisen founded the first cooperative lending banks to support farmers in rural Germany.

While much progress has been made in developing a viable, commercial microfinance sector in the last few decades, several issues remain that need to be addressed before the industry will be able to satisfy massive worldwide demand.

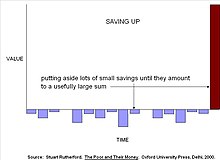

[18] The work of Rutherford, Wright and others has caused practitioners to reconsider a key aspect of the microcredit paradigm: that poor people get out of poverty by borrowing, building microenterprises and increasing their income.

This microfinance project functions as an unofficial banking system where Jyothi, a "deposit collector", collects money from slum dwellers, mostly women, in order for them to accumulate savings.

Customers, on the other hand, may have expenses for travelling to the bank branch, acquiring official documents for the loan application, and loss of time when dealing with the MFI ("opportunity costs").

Indeed, the local microfinance organizations that receive zero-interest loan capital from the online microlending platform Kiva charge average interest and fee rates of 35.21%.

The P2P microlending service Zidisha is based on this premise, facilitating direct interaction between individual lenders and borrowers via an internet community rather than physical offices.

Although it is generally agreed that microfinance practitioners should seek to balance these goals to some extent, there are a wide variety of strategies, ranging from the minimalist profit-orientation of BancoSol in Bolivia to the highly integrated not-for-profit orientation of BRAC in Bangladesh.

Moreover, the attraction of women as a potential investment base is precisely because they are constrained by socio-cultural norms regarding such concepts of obedience, familial duty, household maintenance and passivity.

[37] The result of these norms is that while micro-lending may enable women to improve their daily subsistence to a more steady pace, they will not be able to engage in market-oriented business practice beyond a limited scope of low-skilled, low-earning, informal work.

In particular, the shift in norms such that women continue to be responsible for all the domestic private sphere labour as well as undertaking public economic support for their families, independent of male aid increases rather than decreases burdens on already limited persons.

More recently, the popularity of non-profit global online lending has grown, suggesting that a redress of gender norms might be instituted through individual selection fomented by the processes of such programs, but the reality is as yet uncertain.

[39] This is also due to a general trend for interpersonal microfinance relations to be conducted on grounds of similarity and internal/external recognition: lenders want to see something familiar, something supportable in potential borrowers, so an emphasis on family, goals of education and health, and a commitment to community all achieve positive results from prospective financiers.

The result is that microfinance continues to rely on restrictive gender norms rather than seek to subvert them through economic redress in terms of foundation change: training, business management and financial education are all elements which might be included in parameters of female-aimed loans and until they are the fundamental reality of women as a disadvantaged section of societies in developing states will go untested.

Considering that most bank clients in the developed world need several active accounts to keep their affairs in order, these figures indicate that the task the microfinance movement has set for itself is still very far from finished.

[53] As yet there are no studies that indicate the scale or distribution of 'informal' microfinance organizations like ROSCA's and informal associations that help people manage costs like weddings, funerals and sickness.

Numerous case studies have been published, however, indicating that these organizations, which are generally designed and managed by poor people themselves with little outside help, operate in most countries in the developing world.

Based in Toronto, Ontario, ACCESS is a Canadian charity that helps entrepreneurs without collateral or credit history find affordable small loans.

Momentum provides individuals and families who want to better their financial situation take control of finances, become computer literate, secure employment, borrow and repay loans for business, and purchase homes.

[65] In Canada, microfinancing competes with pay-day loans institutions which take advantage of marginalized and low-income individuals by charging extremely high, predatory interest rates.

Pay day loan companies are unlike traditional microfinance in that they don't encourage collectivism and social capital building in low income communities, however exist solely for profit.

The Network is involved in advocacy on a wide range of issues related to microfinance, micro-enterprises, social and financial exclusion, self-employment and employment creation.

[citation needed] In the summer of 2017, within the framework of the joint project of the Central Bank of Russia and Yandex, a special check mark (a green circle with a tick and Реестр ЦБ РФ 'State MFO Register' text box) appeared search results on the Yandex search engine, informing the consumer that the company's financial services are offered on the marked website, which has the status of a microfinance organization.

[91] The high number of individuals selling similar products and services can cause new entrepreneurs to be subject to cutthroat competition over a demand that has not expanded proportionally with the supply.

She suggests that it happens because of the interplay between the company's mission, the cost differential between poor and unbanked wealthier clients and region specific characteristics pertaining the heterogeneity of their clientele.

CGAP recently commented that: "a large proportion of the money they spend is not effective, either because it gets hung up in unsuccessful and often complicated funding mechanisms (for example, a government apex facility), or it goes to partners that are not held accountable for performance.

In some cases, poorly conceived programs have slowed the development of inclusive financial systems by distorting markets and displacing domestic commercial initiatives with cheap or free money.

"[95] There has also been criticism of microlenders for not taking more responsibility for the working conditions of poor households, particularly when borrowers become quasi-wage labourers, selling crafts or agricultural produce through an organization controlled by the MFI.