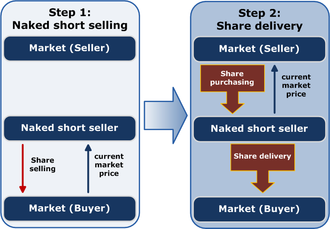

Naked short selling

[2][3] In 2008, the SEC banned what it called "abusive naked short selling"[4] in the United States, as well as some other jurisdictions, as a method of driving down share prices.

[8] Effective September 18, amid claims that aggressive short selling had played a role in the failure of financial giant Lehman Brothers, the SEC extended and expanded the rules to remove exceptions and to cover all companies, including market makers.

[11] Its critics have contended that the practice is susceptible to abuse, can be damaging to targeted companies struggling to raise capital, and has led to numerous bankruptcies.

[citation needed] A Los Angeles Times editorial in July 2008 said that naked short selling "enables speculators to drive down a company's stock by offering an overwhelming number of shares for sale".

Our agency’s rules are highly supportive of short selling, which can help quickly transmit price signals in response to negative information or prospects for a company.

The SEC has stated that the practice can be beneficial in enhancing liquidity in difficult-to-borrow shares, while others have suggested that it adds efficiency to the securities lending market.

[45][46] Japan's Finance Minister, Shōichi Nakagawa stated, "We decided (to move up the short-selling ban) as we thought it could be dangerous for the Tokyo stock market if we do not take action immediately."

[49] The SEC, in describing Regulation SHO, stated that failures to deliver shares that persist for an extended period of time "may result in large delivery obligations where stock settlement occurs".

[49] Regulation SHO also created the "Threshold Security List", which reported any stock where more than 0.5% of a company's total outstanding shares failed delivery for five consecutive days.

'"[15] However, the SEC clarified that appearance on the threshold list "does not necessarily mean that there has been abusive naked short selling or any impermissible trading in the stock".

[60] SEC Chairman Cox noted that the emergency order was "not a response to unbridled naked short selling in financial issues", saying that "that has not occurred".

[68] In July 2009, the SEC, under what the Wall Street Journal described as "intense political pressure", made permanent an interim rule that obliges brokerages to promptly buy or borrow securities when executing a short sale.

The SEC sought information related to two former Refco brokers who handled the account of a client, Amro International, which shorted Sedona's stock.

In December 2006, the SEC sued Gryphon Partners, a hedge fund, for insider trading and naked short-selling involving PIPEs in the unregistered stock of 35 companies.

[73] In March 2007, Goldman Sachs was fined $2 million by the SEC for allowing customers to illegally sell shares short prior to secondary public offerings.

Piper violated securities trading rules from January through May 2005, selling shares without borrowing them, and also failing to "cover short sales in a timely manner", according to the NYSE.

[77] In October 2007, the SEC settled charges against New York hedge fund adviser Sandell Asset Management Corp. and three executives of the firm for, among other things, shorting stock without locating shares to borrow.

[80] In May 2012, lawyers acting for Goldman accidentally released an unredacted document revealing compromising internal discussions regarding naked short selling.

"Fuck the compliance area – procedures, schmecedures", Rolling Stone Magazine quoted Peter Melz, the former president of Merrill Lynch Professional Clearing Corp. as saying in the document.

[6] Referring to trades that remain unsettled, DTCC's chief spokesman Stuart Goldstein said, "We're not saying there is no problem, but to suggest the sky is falling might be a bit overdone.

[95] Pet Quarters alleged the Depository Trust & Clearing Corp.'s stock-borrow program resulted in the creation of nonexistent or phantom stock and contributed to the illegal short selling of the company's shares.

"[11] A study of trading in initial public offerings by two SEC staff economists, published in April 2007, found that excessive numbers of fails to deliver were not correlated with naked short selling.

The paper, which looked at a "unique dataset of the entire cross-section of U.S. equities", credited the initial recognition of strategic delivery fails to Richard Evans, Chris Geczy, David Musto and Adam Reed,[98][99] and found its review to provide evidence consistent with their hypothesis that "market makers strategically fail to deliver shares when borrowing costs are high."

[107] In June 2007, executives of Universal Express, which had claimed naked shorting of its stock, were sanctioned by a federal court judge for violation of securities laws.

"[110] Reviewing the SEC's July 2008 emergency order, Barron's said in an editorial: "Rather than fixing any of the real problems with the agency and its mission, Cox and his fellow commissioners waved a newspaper and swatted the imaginary fly of naked short-selling.

"[14] Holman Jenkins of The Wall Street Journal said the order was "an exercise in symbolic confidence-building" and that naked shorting involved technical concerns except for subscribers to a "devil theory".

[13] The Economist said the SEC had "picked the wrong target", mentioning a study by Arturo Bris of the Swiss International Institute for Management Development who found that trading in the 19 financial stocks became less efficient.

[111] The Washington Post expressed approval of the SEC's decision to address a "frenetic shadow world of postponed promises, borrowed time, obscured paperwork and nail-biting price-watching, usually compressed into a few high-tension days swirling around the decline of a company".

[113] The Wall Street Journal said in an editorial in July 2008 that "the Beltway is shooting the messenger by questioning the price-setting mechanisms for barrels of oil and shares of stock."

[116] In an article published in October 2009, Rolling Stone writer Matt Taibbi contended that Bear Stearns and Lehman Brothers were flooded with "counterfeit stock" that helped kill both companies.