Renewal theory

Instead of exponentially distributed holding times, a renewal process may have any independent and identically distributed (IID) holding times that have finite mean.

A renewal-reward process additionally has a random sequence of rewards incurred at each holding time, which are IID but need not be independent of the holding times.

A renewal process has asymptotic properties analogous to the strong law of large numbers and central limit theorem.

(expected number of arrivals) and reward function

(expected reward value) are of key importance in renewal theory.

The key renewal equation gives the limiting value of the convolution of

Applications include calculating the best strategy for replacing worn-out machinery in a factory; comparing the long-term benefits of different insurance policies; and modelling the transmission of infectious disease, where "One of the most widely adopted means of inference of the reproduction number is via the renewal equation"[1].

In essence, the Poisson process is a continuous-time Markov process on the positive integers (usually starting at zero) which has independent exponentially distributed holding times at each integer

In a renewal process, the holding times need not have an exponential distribution; rather, the holding times may have any distribution on the positive numbers, so long as the holding times are independent and identically distributed (IID) and have finite mean.

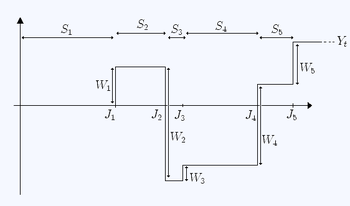

be a sequence of positive independent identically distributed random variables with finite expected value We refer to the random variable

represents the number of jumps that have occurred by time t, and is called a renewal process.

as the random time elapsed between two consecutive events.

For example, if the renewal process is modelling the numbers of breakdown of different machines, then the holding time represents the time between one machine breaking down before another one does.

The Poisson process is the unique renewal process with the Markov property,[2] as the exponential distribution is the unique continuous random variable with the property of memorylessness.

An alternative analogy is that we have a magic goose which lays eggs at intervals (holding times) distributed as

Sometimes it lays golden eggs of random weight, and sometimes it lays toxic eggs (also of random weight) which require responsible (and costly) disposal.

records the total financial "reward" at time t. We define the renewal function as the expected value of the number of jumps observed up to some time

To do this, consider some truncated renewal process where the holding times are defined by

be a function satisfying: The key renewal theorem states that, as

gives as a special case the renewal theorem:[5] The result can be proved using integral equations or by a coupling argument.

[6] Though a special case of the key renewal theorem, it can be used to deduce the full theorem, by considering step functions and then increasing sequences of step functions.

We have almost surely (using the first result and using the law of large numbers on

Renewal processes additionally have a property analogous to the central limit theorem:[7]

That is, for all x > 0 and for all t > 0: where FS is the cumulative distribution function of the IID holding times Si.

The resolution of the paradox is that our sampled distribution at time t is size-biased (see sampling bias), in that the likelihood an interval is chosen is proportional to its size.

However, a renewal interval of average size is not size-biased.

[9] However, the cumulative distribution function of the first inter-event time in the superposition process is given by[10] where Rk(t) and αk > 0 are the CDF of the inter-event times and the arrival rate of process k.[11] Eric the entrepreneur has n machines, each having an operational lifetime uniformly distributed between zero and two years.

Eric may let each machine run until it fails with replacement cost €2600; alternatively he may replace a machine at any time while it is still functional at a cost of €200.

So the overall expected lifetime of the machine is: and the expected cost W per machine is: So by the strong law of large numbers, his long-term average cost per unit time is: then differentiating with respect to t: this implies that the turning points satisfy: and thus We take the only solution t in [0, 2]: t = 2/3.

This is indeed a minimum (and not a maximum) since the cost per unit time tends to infinity as t tends to zero, meaning that the cost is decreasing as t increases, until the point 2/3 where it starts to increase.