Stability and Growth Pact

If a member state breaches the SGP's outlined maximum limit for government deficit and debt, the surveillance and request for corrective action will intensify through the declaration of an Excessive Deficit Procedure (EDP); and if these corrective actions continue to remain absent after multiple warnings, a member state of the eurozone can ultimately also be issued economic sanctions.

The Excessive Deficit Procedure (EDP), also known as the corrective arm of the SGP, was suspended via activation of the "general escape clause" during 2020–2023 to allow for higher deficit spending; first due to the COVID-19 pandemic arriving as an extraordinary circumstance,[8] and later during 2022-2023 due to the Russian invasion of Ukraine having sent energy prices up, defence spending up and budgetary pressures up across the EU.

[12] The EDP will be assessed again starting from 19 June 2024,[13] where each country will have their usual set of a "2024 National Reform Programme" and "2024 Stability or Convergence Programme" analyzed,[14][15] with a compliance check of the 2023 fiscal result and 2024 budget with the existing 2019-version of the SGP rules, although only 3% deficit breaches will be evaluated because no debt limit or debt reduction breach can trigger an EDP in 2024.

[17][18][19] The first "national medium-term fiscal-structural plans" guided by the new revised fiscal rules, will cover the four-year period 2025–2028, and need to be submitted by each member state by 20 September 2024.

[27] In order to stabilise the Eurozone, Member States adopted an extensive package of reforms, aiming at straightening both the substantive budgetary rules and the enforcement framework.

The measures adopted soon proved highly controversial, because they implied an unprecedented curtailment of national sovereignty and the conferral upon the Union of penetrating surveillance competences.

The TSCG was intended to promote the launch of a new intergovernmental economic cooperation, outside the formal framework of the EU treaties, because most (but not all) member states at the time of its creation were willing to be bound by extra commitments.

In line with the existing SGP rules, the European Commission will for each country set the available time-frame for the "adjustment path" until the MTO-limit shall be achieved, based on consideration of a country-specific debt sustainability risk assessment, while also respecting the requirement that the annual improvements for the structural budget balance shall be minimum 0.5% of GDP.

Similar to the general escape clause of the SGP, a state suffering a significant recession or a temporary exceptional event outside its control with major budgetary impact, will be exempted from the requirement to deliver a fiscal automatic correction for as long as it lasts.

[49] Regulation 473/2013 is directed at all eurozone member states and requires a draft budgetary plan for the upcoming year to be submitted annually by 15 October, for a SGP compliance assessment conducted by the European Commission.

The member state shall then await receiving the Commission's opinion before the draft budgetary plan is debated and voted for in their national parliament.

These member states are made subject to even more in depth and frequent "enhanced surveillance", in order to prevent a possible sovereign debt crises to emerge.

Most scholars admit that a considerable improvement occurred in the field of budgetary enforcement, especially for what concerns the imposition of dissuasive sanctions upon noncompliant Members.

Scholars agree in referring the issue of democratic deficit to the lack of a more federalised institutional framework for the Eurozone economic governance.

The argument goes that strongly legitimated Union institutions would avoid the need for penetrating surveillance mechanisms, as they would partially shift economic policymaking at central level.

The latter usually consist in Macroeconomic Adjustment Programs (MAPs) whose adoption is deemed necessary to fix the imbalances which gave rise to the original instability.

[55] In February 2024, the trilogue negotiations between the co-legislators ended with a provisional political agreement on the Commissions proposal for a comprehensive reform of the SGP rules.

[56][57][19] The first "national medium-term fiscal-structural plans" guided by the new revised fiscal rules, will cover the four-year period 2025-2028, and need to be submitted by each member state by 20 September 2024.

[12] The EDP will be assessed again starting from 19 June 2024,[13] where each country will have their usual set of a "2024 National Reform Programme" and "2024 Stability or Convergence Programme" analyzed,[14][15] with a compliance check of the 2023 fiscal result and 2024 budget with the existing 2019-version of the SGP rules; although only 3% deficit breaches will be evaluated - because no debt limit or debt reduction breach can trigger an EDP in 2024.

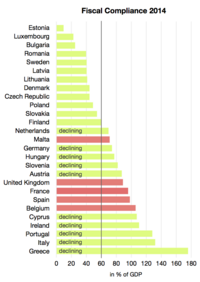

"[12] 10 out of 27 member states (Belgium, Czechia, France, Hungary, Italy, Malta, Poland, Romania, Slovakia and Spain) had a technical deficit-based "SGP criteria breach" as per their 2023 fiscal results published by Eurostat in April 2024.

[47] Across the first seven years, since the entry into force of the Stability and Growth Pact, all EU Member States were required to strive towards a common MTO being "to achieve a budgetary position of close to balance or in surplus over a complete business cycle – while providing a safety margin towards continuously respecting the government's 3% deficit limit".

In order to ensure long-term compliance with the SGP deficit and debt criteria, the member states have since the SGP-reform in March 2005 striven towards achieving their country-specific Medium-Term budgetary Objective (MTO).

The "minimum MTO" that the "nationally selected MTO" needs to respect, is equal to the strictest of the following three limits (which since a method change in 2012 now automatically is rounded to the lowest 1⁄4-value, if calculated to a figure with the last two digits after punctuation differing from 00/25/50/75, i.e. -0.51% will be rounded to -0.75%[77]): (1) MTOMB (the Minimum Benchmark, adds a public budget safety margin to ensure the 3%-limit will be respected during economic downturns) (2) MTOILD (the minimum value ensuring long-term sustainability of public budgets taking into account the Implicit Liabilities and Debt, aiming to ensure convergence across a long-term horizon of debt ratios towards prudent levels below 60% with due consideration to the forecast budgetary impact of ageing populations) (3) MTOea/erm2/fc (Council Regulation 1466/97 of the SGP explicitly defined a -1.0% limit applying for eurozone states or ERM2 members already in 2005; but if having committed to a stricter requirement through ratification and bound acceptance of Title III of the Fiscal Compact, a stricter -0.5% limit will replace it whenever the debt-to-GDP ratio of the member state exceeds 60%).

The third minimum limit listed above (MTOea/erm2/fc), mean that EU member states having ratified the Fiscal Compact and being bound by its fiscal provisions in Title III (which requires a special additional declaration of intent for non-eurozone member states), are obliged to select a MTO which does not exceed a structural deficit of 1.0% of GDP at maximum if they have a debt-to-GDP ratio significantly below 60%, and of 0.5% of GDP maximum if they have a debt-to-GDP ratio above 60%.

The Minimum MTOs are recalculated every third year by the Economic and Financial Committee, based on the above-described procedure and formulas, that among others require the prior publication of the commission's triennial Ageing Report.

The MTOILD limits for Belgium, Denmark, Hungary and the Netherlands were revised in 2013, due to the impact of their 2012 pension reforms only subsequently being incorporated for some updated S2COA values in the Commission's Fiscal Sustainability Report 2012 released on 18 December 2012.

Except from the situation where a member state request an extraordinary recalculation of its MTOILD (due to implementation of major structural reforms), all calculated "Minimum MTOs" will however remain frozen for the entire three‑year period it covers, and not be changed by the annually revised MTOMB.

[438] The problem is, that countries in the EMU cannot react to economic shocks with a change of their monetary policy since it is coordinated by the ECB and not by national central banks.

The Pact has proved to be unenforceable against big countries that dominate the EU economically, such as France and Germany, which were its strongest promoters when it was created.

The reasons that larger countries have not been punished include their influence and large number of votes on the Council, which must approve sanctions; their greater resistance to "naming and shaming" tactics, since their electorates tend to be less concerned by their perceptions in the European Union; their weaker commitment to the euro compared to smaller states; and the greater role of government spending in their larger and more enclosed economies.