Too big to fail

Congressman Stewart McKinney in a 1984 Congressional hearing, discussing the Federal Deposit Insurance Corporation's intervention with Continental Illinois.

Common means of avoiding failure include facilitating a merger, providing credit, or injecting government capital, all of which protect at least some creditors who otherwise would have suffered losses.

[21][22] Fed Chair Ben Bernanke described in November 2013 how the Panic of 1907 was essentially a run on the non-depository financial system, with many parallels to the crisis of 2008.

Regulators shunned this third option for many years, fearing that if regionally or nationally important banks were thought generally immune to liquidation, markets in their shares would be distorted.

[25] The Federal Deposit Insurance Corporation Improvement Act was passed in 1991, giving the FDIC the responsibility to rescue an insolvent bank by the least costly method.

"[30] Research has shown that banking organizations are willing to pay an added premium for mergers that will put them over the asset sizes that are commonly viewed as the thresholds for being too big to fail.

[33][34][35] Another study by Frederic Schweikhard and Zoe Tsesmelidakis[36] estimated the amount saved by America's biggest banks from having a perceived safety net of a government bailout was $120 billion from 2007 to 2010.

[37] One 2013 study (Acharya, Anginer, and Warburton) measured the funding cost advantage provided by implicit government support to large financial institutions.

[39] During November 2013, the Moody's credit rating agency reported that it would no longer assume the eight largest U.S. banks would receive government support in the event they faced bankruptcy.

However, the GAO reported that politicians and regulators would still face significant pressure to bail out large banks and their creditors in the event of a financial crisis.

[40] Some critics have argued that "The way things are now banks reap profits if their trades pan out, but taxpayers can be stuck picking up the tab if their big bets sink the company.

"[41] Additionally, as discussed by Senator Bernie Sanders, if taxpayers are contributing to rescue these companies from bankruptcy, they "should be rewarded for assuming the risk by sharing in the gains that result from this government bailout".

[44] On March 6, 2013, then United States Attorney General Eric Holder testified to the Senate Judiciary Committee that the size of large financial institutions has made it difficult for the Justice Department to bring criminal charges when they are suspected of crimes, because such charges can threaten the existence of a bank and therefore their interconnectedness may endanger the national or global economy.

In this he contradicted earlier written testimony from a deputy assistant attorney general, who defended the Justice Department's "vigorous enforcement against wrongdoing".

[48] Other conservatives including Thomas Hoenig, Ed Prescott, Glenn Hubbard, and David Vitter also advocated breaking up the largest banks,[49] but liberal commentator Matthew Yglesias questioned their motives and the existence of a true bipartisan consensus.

"[52] Kareem Serageldin pleaded guilty on November 22, 2013, for his role in inflating the value of mortgage bonds as the housing market collapsed, and was sentenced to two and a half years in prison.

[53][54] As of April 30, 2014, Serageldin remains the "only Wall Street executive prosecuted as a result of the financial crisis" that triggered the Great Recession.

[55] The much smaller Abacus Federal Savings Bank was prosecuted (but exonerated after a jury trial) for selling fraudulent mortgages to Fannie Mae.

[58] The United States passed the Dodd–Frank Act in July 2010 to help strengthen regulation of the financial system in the wake of the subprime mortgage crisis that began in 2007.

Such measures for preventing the New Darwinism of the survival of the fittest and the politically best connected should be distinguished from regulatory interventions based on the narrow leverage ratio aimed at regulating risk (regardless of size, except for a de minimis lower limit).

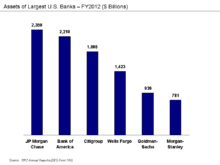

As of 2022, these are:[65] *Note: In the wake of the 2023 banking crisis, the Swiss government facilitated an acquisition of Credit Suisse by UBS to avoid the former's collapse.

UBS completed the acquisition in June 2023, thereby making Credit Suisse the first failure of a bank considered "too big to fail" since the Global Financial Crisis.

[38][57][67] On March 6, 2013, United States Attorney General Eric Holder told the Senate Judiciary Committee that the Justice Department faces difficulty charging large banks with crimes because of the risk to the economy.

He added, "I don't think merely raising the fees or capital on large institutions or taxing them is enough ... they'll absorb that, they'll work with that, and it's totally inefficient and they'll still be using the savings.

"[9] On April 10, 2013, International Monetary Fund managing director Christine Lagarde told the Economic Club of New York "too big to fail" banks had become "more dangerous than ever" and had to be controlled with "comprehensive and clear regulation [and] more intensive and intrusive supervision".

[74] When Penn Square failed in July 1982, the Continental's distress became acute, culminating with press rumors of failure and an investor-and-depositor run in early May 1984.

Besides generic concerns of size, contagion of depositor panic and bank distress, regulators feared the significant disruption of national payment and settlement systems.

In a United States Senate hearing afterwards, the then Comptroller of the Currency C. T. Conover defended his position by admitting the regulators will not let the largest 11 banks fail.

The firm's master hedge fund, Long-Term capital Portfolio L.P., collapsed in the late 1990s, leading to an agreement on September 23, 1998, among 14 financial institutions for a $3.6 billion recapitalization (bailout) under the supervision of the Federal Reserve.

Members of LTCM's board of directors included Myron S. Scholes and Robert C. Merton, who shared the 1997 Nobel Memorial Prize in Economic Sciences for a "new method to determine the value of derivatives".