Constant proportion portfolio insurance

Constant proportion portfolio investment (CPPI) is a trading strategy that allows an investor to maintain an exposure to the upside potential of a risky asset while providing a capital guarantee against downside risk.

CPPI products on a variety of risky assets have been sold by financial institutions, including equity indices and credit default swap indices.

[4] In order to guarantee the capital invested, the seller of portfolio insurance maintains a position in a treasury bonds or liquid monetary instruments, together with a leveraged position in an "active asset", which constitutes the performance engine.

While in the case of a bond+call, the client would only get the remaining proceeds (or initial cushion) invested in an option, bought once and for all, the CPPI provides leverage through a multiplier.

This multiplier is set to 100 divided by the crash size (as a percentage) that is being insured against.

The allocation to the risky asset may vary during the life of the product.

Should the exposure to the risky asset drop to zero or a very low level, then the CPPI is said to be deleveraged or cashed out.

The CPPI strategy will then be fully allocated to the low risk asset until the product matures.

CPPI strategies aim at offering a capital protection to its investors.

The benefit is that CPPI protection is much cheaper and less impacted by market movements.

The bond floor is the value below which the value of the CPPI portfolio should never fall in order to be able to ensure the payment of all future due cash flows (including notional guarantee at maturity).

A measure of the proportion of the equity part compared to the cushion, or (CPPI-bond floor)/equity.

Theoretically, this should equal 1/multiplier and the investor uses periodic rebalancing of the portfolio to attempt to maintain this.

If the gap remains between an upper and a lower trigger band (resp.

It effectively reduces transaction costs, but the drawback is that whenever a trade event to reallocate the weights to the theoretical values happen, the prices have either shifted quite a bit high or low, resulting in the CPPI effectively buying (due to leverage) high and selling low.

As dynamic trading strategies assume that capital markets trade in a continuous fashion, gap risk is the main concern of CPPI writer, since a sudden drop in the risky underlying trading instrument(s) could reduce the overall CPPI net asset value below the value of the bond floor needed to guarantee the capital at maturity.

In the models initially introduced by Black and Jones[2] Black & Rouhani,[3] this risk does not materialize: to measure it one needs to take into account sudden moves (jumps) in prices.

[5] Such sudden price moves may make it impossible to shift the position from the risky assets to the bond, leading the structure to a state where it is impossible to guarantee principal at maturity.

With this feature being ensured by contract with the buyer, the writer has to put up money of his own to cover for the difference (the issuer has effectively written a put option on the structure NAV).

Banks generally charge a small "protection" or "gap" fee to cover this risk, usually as a function of the notional leveraged exposure.

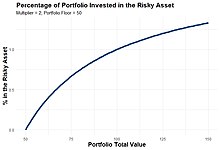

Because the percentage of the portfolio invested in the risky asset at any given time can vary, the dynamics of a CPPI strategy are complex.

The average return and variance of a CPPI strategy across investment period