Customer Profitability Analysis

Equally, research suggests that credit score does not necessarily impact the lenders' profitability.

[citation needed] Management accounting systems often focus on products, departments, or geographic regions, but not on customers.

[1] Once costs are matched with customer revenues, segments of differing profitability can be discovered.

[2] The main purpose of CPA is to provide to organization management with the understanding of each customer profitability.

Companies most typically have no trouble finding out the amount of revenue attributed to a particular customer, thus article will not cover this aspect.

Possessing information defined above in "Input" chapter, management / accounting team can execute various different calculations, rankings, and comparisons between different customers / customer segments, necessary to reaching further conclusions and taking action.

CPA therefore allows the company to uncover groups of customers that will likely respond best to profit improvement programs.

Below are few examples from available literature, nonetheless each company may apply another strategy, better fitting into this particular organization business model, by either modifying below mentioned methods, or employing completely new ones.

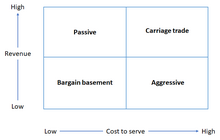

Finally, the last quadrant (aggressive) is listing customers generating high costs and bringing low revenue.

For example: This 4-boxes (matrix of customer profitability and strategy alignment) method was suggested by several literature positions.