Dodd–Frank Wall Street Reform and Consumer Protection Act

The Dodd–Frank Wall Street Reform and Consumer Protection Act, commonly referred to as Dodd–Frank, is a United States federal law that was enacted on July 21, 2010.

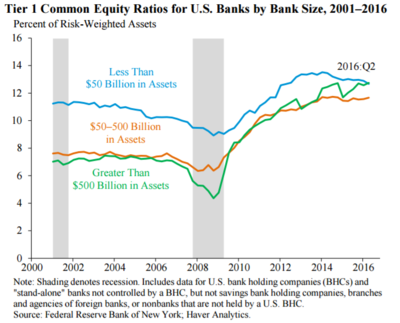

[8][9] In 2017, Federal Reserve Chairwoman Janet Yellen stated that "the balance of research suggests that the core reforms we have put in place have substantially boosted resilience without unduly limiting credit availability or economic growth.

[19] In June 2009, President Obama introduced a proposal for a "sweeping overhaul of the United States financial regulatory system, a transformation on a scale not seen since the reforms that followed the Great Depression".

This rule was unsuccessfully challenged in conference committee by Chris Dodd, who—under pressure from the White House[32]—submitted an amendment limiting that access and ability to nominate directors only to single shareholders who have over 5 percent of the company and have held the stock for at least two years.

[31] The "Durbin amendment"[33] is a provision in the final bill aimed at reducing debit card interchange fees for merchants and increasing competition in payment processing.

[56] The Dodd-Frank Wall Street Reform and Consumer Protection Act is categorized into 16 titles and, by one law firm's count, it requires that regulators create 243 rules, conduct 67 studies, and issue 22 periodic reports.

[58]The Act changes the existing regulatory structure, by creating a number of new agencies (while merging and removing others) in an effort to streamline the regulatory process, increasing oversight of specific institutions regarded as a systemic risk, amending the Federal Reserve Act, promoting transparency, and additional changes.

The Act's intentions are to provide rigorous standards and supervision to protect the economy and American consumers, investors and businesses; end taxpayer-funded bailouts of financial institutions; provide for an advanced warning system on the stability of the economy; create new rules on executive compensation and corporate governance; and eliminate certain loopholes that led to the 2008 economic recession.

The institutions affected by these changes include most of the regulatory agencies currently involved in monitoring the financial system (Federal Deposit Insurance Corporation (FDIC), U.S. Securities and Exchange Commission (SEC), Office of the Comptroller of the Currency (OCC), Federal Reserve (the "Fed"), the Securities Investor Protection Corporation (SIPC), etc.

The act eliminates that exemption, rendering numerous additional investment advisers, hedge funds, and private equity firms subject to new registration requirements.

A 2019 study found that this switch in enforcement to state regulators increased misconduct among investment advisers by thirty to forty percent, with a bigger increase in areas with less sophisticated clients, less competition, and among advisers with more conflicts of interest, most likely because on average state regulators have less resources and enforcement capacity compared to the SEC.

[65] Dodd felt it would be a "huge mistake" to craft the bill under the auspices of bipartisan compromise stating "(y)ou're given very few moments in history to make this kind of a difference, and we're trying to do that."

"[66] During a Senate Republican press conference on April 21, 2010, Richard Shelby reported that he and Dodd were meeting "every day" and were attempting to forge a bipartisan bill.

Kay Bailey Hutchison indicated her desire to see state banks have access to the Fed, while Orrin Hatch had concerns over transparency, and the lack of Fannie and Freddie reform.

[69] Ed Yingling, president of the American Bankers Association, regarded the reforms as haphazard and dangerous, saying, "To some degree, it looks like they're just blowing up everything for the sake of change.

[70] A survey by Rimes Technologies Corp of senior investment banking figures in the U.S. and UK showed that 86 percent expect that Dodd–Frank will significantly increase the cost of their data operations.

[72] Continental European scholars have also discussed the necessity of far-reaching banking reforms in light of the current crisis of confidence, recommending the adoption of binding regulations that would go further than Dodd–Frank—notably in France where SFAF and World Pensions Council (WPC) [fr] banking experts have argued that, beyond national legislations, such rules should be adopted and implemented within the broader context of separation of powers in European Union law.

[73][74] This perspective has gained ground after the unraveling of the Libor scandal in July 2012, with mainstream opinion leaders such as the Financial Times editorialists calling for the adoption of an EU-wide "Glass Steagall II".

[75] An editorial in the Wall Street Journal speculated that the law would make it more expensive for startups to raise capital and create new jobs;[76] other opinion pieces suggest that such an impact would be due to a reduction in fraud or other misconduct.

[79] Public companies will have to work to adopt new policies in order to adapt to the changing regulatory environment they will face over the coming years.

[82] In addition, companies are required to disclose any golden parachute compensation that may be paid out to executives in the case of a merger, acquisition, or sale of major assets.

[80] In addition, the provisions in this section prevent brokers from voting on any major corporate governance issue as determined by the SEC including the election of board members.

[84] Additional provisions set forth by Dodd–Frank in section 972 require public companies to disclose in proxy statements reasons for why the current CEO and chairman of the board hold their positions.

[80] Under new regulations any whistleblowers who voluntarily expose inappropriate behavior in public corporations can be rewarded with substantial compensation and will have their jobs protected.

[95][96] On January 14, 2019, the Supreme Court refused to review the District of Columbia Circuit's decision to dismiss their challenge to the constitutionality of the CFPB's structure as an "independent" agency.

These researchers believed that regulatory barriers fell most heavily on small banks, even though legislators intended to target large financial institutions.

[106] According to Federal Reserve Chairwoman Janet Yellen in August 2017, "The balance of research suggests that the core reforms we have put in place have substantially boosted resilience without unduly limiting credit availability or economic growth.

While he states that "the overall pattern of the legislation is disturbing," he also concludes that some are clearly helpful, such as the derivatives exchanges and the Consumer Financial Protection Bureau.

[110] Regarding the Republican-led rollback of some provisions of Dodd–Frank in 2018, this move from increased regulation after a crisis to deregulation during an economic boom has been a recurrent feature in the United States.

[111] The SEC's 2017 annual report on the Dodd–Frank whistleblower program stated: "Since the program's inception, the SEC has ordered wrongdoers in enforcement matters involving whistleblower information to pay over $975 million in total monetary sanctions, including more than $671 million in disgorgement of ill-gotten gains and interest, the majority of which has been...returned to harmed investors."