Economic history of Turkey

[1] At the time of the collapse of the Ottoman Empire (see Economy of the Ottoman Empire) during World War I and the subsequent birth of the Republic, the Turkish economy was underdeveloped: agriculture depended on outmoded techniques and poor-quality livestock, and Turkey's industrial base was weak; the few factories producing basic products such as sugar and flour were under foreign control as a result of the capitulations.

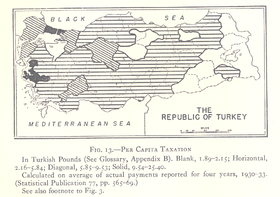

Industry and services grew at more than nine percent per year from 1923 to 1929; however, their share of the economy remained quite low at the end of the decade[citation needed].

[4] In 1930, the Turkish government established the Central Bank of the Republic of Turkey, which was responsible for the formulation of monetary policies and the regulation of money supply.

[4] Coping with the negative impact of the western economic crisis from 1929 to 1933 on the Turkish economy is the direct cause of the implementation of the nationalist policy in Turkey.

During the 1940s, the economy stagnated, in large part because maintaining armed neutrality during World War II increased the country's military expenditures while almost entirely curtailing foreign trade.

In each case, an industry-led period of rapid expansion, marked by a sharp increase in imports, resulted in a balance of payments crisis.

Devaluations of the Turkish lira and austerity programs designed to dampen domestic demand for foreign goods were implemented in accordance with International Monetary Fund guidelines.

These measures usually led to sufficient improvement in the country's external accounts to make possible the resumption of loans to Turkey by foreign creditors.

Investment in the state-owned economy is mainly concentrated in large enterprises that are capital – and technology-intensive, such as infrastructure construction and metallurgy and chemical industry.

The investment sector of the private economy is mainly small and medium-sized enterprises that produce daily consumer goods such as food processing and textiles.

Turkish authorities had failed to take sufficient measures to adjust to the effects of the sharp increase in world oil prices in 1973–74 and had financed the resulting deficits with short-term loans from foreign lenders.

By 1979 inflation had reached triple-digit levels, unemployment had risen to about 15 percent, the industry was using only half its capacity, and the government was unable to pay even the interest on foreign loans.

In the year after the military coup, Özal's economic recovery plan was initially implemented, and the inflation rate fell from 140% to 35%.

The government pursued these goals by means of a comprehensive package: devaluation of the Turkish lira and institution of flexible exchange rates, maintenance of positive real interest rates and tight control of the money supply and credit, elimination of most subsidies and the freeing of prices charged by state enterprises, reform of the tax system, and encouragement of foreign investment.

The liberalization program overcame the balance of payments crisis, reestablished Turkey's ability to borrow in international capital markets, and led to renewed economic growth.

The rapid resurgence of growth and the improvement in the balance of payments were insufficient to overcome unemployment and inflation, which remained serious problems.

[13] With limited access to the Persian Gulf, Iraq also came to depend heavily on Turkey for export routes for its crude oil.

Iraq had financed two pipelines located next to one another from its northern Kirkuk oilfields to the Turkish Mediterranean port of Yumurtalık, slightly northwest of İskenderun.

Saudi Arabia, Kuwait, and the United Arab Emirates (UAE) moved to compensate Turkey for these losses, however, and by 1992 the economy again began to grow rapidly.

External and internal confidence in the government's ability to manage the impending balance of payments crisis waned, compounding economic difficulties.

Mounting concern over the disarray in economic policy was reflected in an accelerated "dollarization" of the economy as residents switched domestic assets into foreign-currency deposits to protect their investments.

The downgrading by credit-rating agencies and a lack of confidence in the government's budget deficit target of 14 percent of GDP for 1994 triggered large-scale capital flight and the collapse of the exchange rate.

[14] The package of measures announced by the government on April 5, 1994, was also submitted to the IMF as part of its request for a US$740 million standby facility beginning in July 1994.

The slowdown in government spending, a sharp loss in business confidence, and the resulting decline in economic activity reduced tax revenues, however.

Analysts pointed out that despite the fragility of the macroeconomic adjustment process and the susceptibility of fiscal policy to political pressures, the government continued to be subject to market checks and balances.

Combined with a stronger private sector, particularly on the export front, the economy was expected to bounce back to a pattern of faster growth.

[15] A comprehensive research in Journal of Developing Economies which was authored by Mete Feridun of University of Greenwich Business School, report statistical evidence that currency crises in Turkey during this period are associated with global liquidity conditions, fiscal imbalances, capital outflows, and banking sector weaknesses [16] A more recent research by Mete Feridun which was published in Emerging Markets Finance and Trade investigates the hypothesis that there is a causal relation between speculative pressure and real exchange rate overvaluation, banking-sector fragility, and the level of international reserves in Turkey shedding more light on Turkey's economic history of 1990s.

[19] Turkey's location at the crossroads of Europe, Asia, and the Middle East has made it a strategic hub for trade and investment, but also a vulnerable target for economic turmoil.

This growth was largely driven by a series of structural reforms initiated by the AKP government, including the privatization of state-owned enterprises, deregulation of key sectors, and improvements in fiscal and monetary policies.

The lira has also experienced significant depreciation against major currencies, leading to a rise in foreign debt and a decline in purchasing power for Turkish citizens.