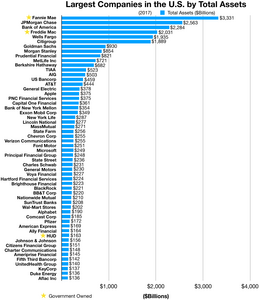

Fannie Mae

The Federal National Mortgage Association (FNMA), commonly known as Fannie Mae, is a United States government-sponsored enterprise (GSE) and, since 1968, a publicly traded company.

To address this, Fannie Mae was established by the U.S. Congress in 1938 by amendments to the National Housing Act[9] as part of Franklin Delano Roosevelt's New Deal.

[19] The Act amended the charter of Fannie Mae and Freddie Mac to reflect the Democratic Congress' view that the GSEs "have an affirmative obligation to facilitate the financing of affordable housing for low- and moderate-income families in a manner consistent with their overall public purposes, while maintaining a strong financial condition and a reasonable economic return".

We sought to bring the standards we apply to the prime space to the subprime market with our industry partners primarily to expand our services to underserved families.

For example, Tom Lund, the head of our single-family mortgage business, publicly stated, "One of the things we don't feel good about right now as we look into this marketplace is more homebuyers being put into programs that have more risk.

[27] Nassim Taleb wrote in The Black Swan: "The government-sponsored institution Fannie Mae, when I look at its risks, seems to be sitting on a barrel of dynamite, vulnerable to the slightest hiccup.

[29] The Senate legislation was an effort to reform the existing GSE regulatory structure in light of the recent accounting problems and questionable management actions leading to considerable income restatements by the GSEs.

[29] Sen. John McCain's decision to become a cosponsor of S.190 almost a year later in 2006 was the last action taken regarding Sen. Hagel's bill in spite of developments since clearing the Senate Committee.

McCain pointed out that Fannie Mae's regulator reported that profits were "illusions deliberately and systematically created by the company's senior management" in his floor statement giving support to S.190.

[33] Following their mission to meet federal Housing and Urban Development (HUD) housing goals, GSEs such as Fannie Mae, Freddie Mac and the Federal Home Loan Banks (FHLBanks) had striven to improve home ownership of low and middle income families, underserved areas, and generally through special affordable methods such as "the ability to obtain a 30-year fixed-rate mortgage with a low down payment ... and the continuous availability of mortgage credit under a wide range of economic conditions".

[35] The market shifted away from regulated GSEs and radically toward Mortgage Backed Securities (MBS) issued by unregulated private-label securitization (PLS) conduits, typically operated by investment banks.

The shift toward riskier mortgages and private label MBS distribution occurred as financial institutions sought to maintain earnings levels that had been elevated during 2001–2003 by an unprecedented refinancing boom due to historically low interest rates.

In July 2008, the government attempted to ease market fears by reiterating their view that "Fannie Mae and Freddie Mac play a central role in the US housing finance system".

[36] Fannie Mae and smaller Freddie Mac owned or guaranteed a massive proportion of all home loans in the United States and so were especially hard hit by the slump.

Paulson's plan was to go in swiftly and seize the two GSEs, rather than provide loans as he did for AIG and the major banks; he told president Bush that "the first sound they hear will be their heads hitting the floor", in a reference to the French Revolution.

[43][44][45][46][47][48][49] The authority of the U.S. Treasury to advance funds for the purpose of stabilizing Fannie Mae, or Freddie Mac is limited only by the amount of debt that the entire federal government is permitted by law to commit to.

The July 30, 2008, law enabling expanded regulatory authority over Fannie Mae and Freddie Mac increased the national debt ceiling by US$800 billion (equivalent to $1,111,800,000,000 in 2023), to a total of US$10.7 trillion in anticipation of the potential need for the Treasury to have the flexibility to support the federal home loan banks.

[56][57][58][59] On May 11, 2015 The Wall Street Journal reported that A U.S. District Court judge said Nomura Holdings Inc. was not truthful in describing mortgage-backed securities sold to Fannie Mae and Freddie Mac, giving a victory to the companies' conservator, the Federal Housing Finance Agency (FHFA).

Judge Denise Cote asked the FHFA to propose updated damages to be paid by Nomura and co-defendant RBS Securities Inc., which underwrote some of the investments.

In her decision, Judge Cote wrote that Nomura, in offering documents for mortgage-backed securities sold to Fannie and Freddie, didn't accurately describe the loans' quality.

Nomura and RBS were two of 18 financial institutions, including Bank of America Corp. and Goldman Sachs Group Inc., targeted in 2011 by the FHFA, which alleged that the companies lied about the quality of the loans underlying the securities.

[63] By purchasing the mortgages, Fannie Mae and Freddie Mac provide banks and other financial institutions with fresh money to make new loans.

The conforming loan limit for Fannie Mae, along with Freddie Mac, is set by Office of Federal Housing Enterprise Oversight (OFHEO), the regulator of both GSEs.

After 8 years of litigation, in 2012, a summary judgment was issued clearing the trio, indicating the government had insufficient evidence that would enable any jury to find the defendants guilty.

[78] In June 2008, The Wall Street Journal reported that two former CEOs of Fannie Mae, James A. Johnson and Franklin Raines, had received loans below market rate from Countrywide Financial.

[81] "The SEC alleges they 'knew and approved of' misleading statements claiming the companies had minimal exposure to subprime loans at the height of home mortgage bubble.

"[82] Former Freddie chief financial officer Anthony "Buddy" Piszel, who in February 2011, was CFO of CoreLogic, "had received a notice from the SEC that the agency was considering taking action against him".

JPMorgan Chase was one of 18 financial institutions the FHFA sued back in 2011, accusing them of selling to Fannie and Freddie securities that "had different and more risky characteristics than the descriptions contained in the marketing and sales materials".

Swiss lender UBS has already reached an $885 million settlement with the FHFA in connection with losses Fannie and Freddie sustained on over $6.4 billion worth of mortgage securities.

[84] On May 29, 2013, the Los Angeles Times reported that a former foreclosure specialist at Fannie Mae has been charged but pleaded "not guilty" to accepting a kickback from an Arizona real estate broker in a Santa Ana Federal court.