Penn Central Transportation Company

While railroads elsewhere in North America drew revenues from long-distance shipments of commodities such as coal, lumber, paper and iron ore, railroads in the densely-populated northeast traditionally depended on a heterogeneous mix of services, including: These labor-intensive, short-haul services proved vulnerable to competition from automobiles, buses, and trucks, a threat recently invigorated by the new limited-access highways authorized in the Federal-Aid Highway Act of 1956.

Changes to passenger fares and freight shipment rates required approval from the capricious Interstate Commerce Commission (ICC), as did mergers or abandonment of lines.

As that revenue stream faded following WWII, neither could slim their assets fast enough to earn a substantial profit (although the NYC came much closer).

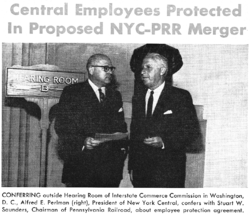

[2]: 215 Neither railroad had much respect for its merger partner; the lines had fought bitterly over New York-Chicago custom and ill-will remained in the executive suites.

[2]: 248 Saunders later commented: "Because of the many years it took to consummate the merger, the morale of both railroads was badly disrupted and they were faced with unmanageable problems which were insurmountable.

"[5] Almost immediately after the transaction cleared, the organizational headwinds presaged during the merger negotiations began to overwhelm the new corporation's management.

[2]: 248 Clashing union contracts prevented the company's left hand from talking to its right,[6]: 233–234 and incompatible computer systems meant that PC classification clerks regularly lost track of train movements.

Derailments and wrecks occurred regularly; when the trains avoided mishap, they operated far below design speed, resulting in delayed shipments and excessive overtime.

In 1969, most of Maine's potato production rotted in the PC's Selkirk Yard, hurting the Bangor & Aroostook Railroad, whose shippers vowed never to ship by rail again.

[citation needed] As PC's management struggled to wrestle the company into submission, the structural headwinds facing all northeastern railroads continued unabated.

[2] Penn Central's executives tried to diversify the troubled firm into real estate and other non-railroad ventures, but in a slow economy these businesses performed little better than the original railroad assets.

To create the illusion of success, management also insisted on paying dividends to shareholders, desperately borrowing funds to buy time for the business to turn around.

George Drury described the bankruptcy as "a cataclysmic event, both to the railroad industry and to the nation's business community,"[2]: 250 not least because Penn Central increasingly appeared the proverbial canary in the coal mine.

The Rock Island, midway through a decade spent arguing with regulators about a merger, was stumbling towards another stunning bankruptcy, as was the Milwaukee Road, the nation's most technologically advanced transcontinental.

The search for a new president was concluded when the Southern Railway's, Graham Claytor offered up William H. "Wild Bill" Moore to head the company.

Moore had been a protégé of the previous Southern president, D. William Brosnan who had been known for both cutting costs, and for routinely firing workers on the spot.

[8] In 1972, the damage from Hurricane Agnes destroyed important Penn Central branches and main lines,[11] and pushed the other northeastern roads into bankruptcy.

DOT), Penn Central agreed to trial new technologies to revive the flagging passenger services on what would become the Northeast Corridor.

The 1980 Staggers Act, which deregulated the railroad industry, proved to be a key factor in bringing Conrail and the old PC assets back to life.

In the 1970s and 1980s, the company now called The Penn Central Corporation was a small conglomerate that largely consisted of the diversified sub-firms it had before the crash.

Though the company retained ownership of some rights-of-way and station properties connected with the railroads, it continued to liquidate these and eventually concentrated on one of its subsidiaries in the insurance business.

Until late 2006, American Financial Group still owned Grand Central Terminal, though all railroad operations were managed by the Metropolitan Transportation Authority (MTA).

[19] The MTA paid $2.4 million annually in rent in 2007 and had an option to buy the station and tracks in 2017, although Argent could extend the date another 15 years to 2032.

[18] The assets included the 156 miles (251 km) of rail used by the Hudson and Harlem Lines, and Grand Central Terminal, as well as unused development rights above the tracks in Midtown Manhattan.

[18] In November 2018, the MTA proposed purchasing the Hudson and Harlem Lines as well as the Grand Central Terminal for up to $35.065 million, plus a discount rate of 6.25%.

The purchase would include all inventory, operations, improvements, and maintenance associated with each asset, except for the air rights over Grand Central.