Pigouvian tax

A Pigouvian tax is a method that tries to internalize negative externalities to achieve the Nash equilibrium and optimal Pareto efficiency.

[2] Often-cited examples of negative externalities are environmental pollution and increased public healthcare costs associated with tobacco and sugary drink consumption.

[4][5] An example sometimes cited is a subsidy for the provision of flu vaccines and the public goods (such as education and national defense), research & development, etc.

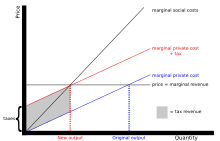

If the tax is placed on the quantity of emissions from the factory, the producers have an incentive to reduce output to the socially optimum level.

If the tax is placed on the percentage of emissions per unit of production, the factory has the incentive to change to cleaner processes or technology.

It is generally accepted now that the magnitude of the "revenue-recycling" benefit is lower than the 20–50 cents per dollar of revenue, but there are differing views on whether the second effect is positive or negative.

The line of argument suggesting that the second "benefit" is negative proposes a previously unrecognized "tax interaction effect" (Bovenberg and de Mooij 1994).

[14] They define the double-dividend hypothesis as the theory that environmental taxes can improve the environment and increase economic efficiency simultaneously.

Fullerton and Metcalf also mention that the effectiveness of any sort of Pigouvian tax depends on whether it supplements or replaces an existing pollution regulation.

In the real world, second-best case, the status quo includes an income tax that distorts the labor supply.

But because C's price has not changed and it can substitute for D, consumers will buy C instead of D. Suddenly the government's environmental tax base has eroded and its revenue with it.

This rejection of the double dividend hypothesis found in the "tax interaction" literature was met with surprise and skepticism among economists for a variety of reasons.

There are multiple sources of ambiguity, differing definitions of what constitutes a 'double dividend', and confusion caused when comparing models with direct versus indirect tax programs, reliance on comparisons with an unreliable benchmark, and misinterpretation of notation in the literature.

[17] In retrospect, three factors contributed to misleading interpretations in the TI literature: an algebraic error, the use of an unreliable benchmark, and unrecognized compounding or double taxation.

As a result, the conclusion that a large, previously unnoticed distortionary tax interaction effect existed can be seen as partly due to misinterpretations (Jaeger 2013).

[18] Despite these sources of confusion, it remains the case that a) the possibility of a double dividend depends on specifics specific to the demands and the economy in which an environmental tax is being considered, and b) that the efficiency gains with revenue recycling will be greater, potentially significantly greater, than when revenues are not collected and used to reduce pre-existing revenue-raising taxes.

Indeed, the joint pursuit of these two goals through taxation can enable the government to justify doing more of each by making the optimal environmental tax higher than it would be otherwise, and by lowering the distortionary cost of financing the provision of public goods.

[20] Economist Ronald Coase argued that individuals can come to an agreement with an efficient result without the need for a third party when transaction costs are low.

Yet, in dynamic settings Coasean bargaining ex post may lead to inefficient investments ex ante (the so-called hold-up problem).

[25] The authors include an example of the U.S. regulations in coal-fired electrical power plants that require the reduction of 10 million tons of sulfur dioxide emissions.

[29] Since 1963, when William Vickrey published a paper and called for the pricing of traffic based on the welfare economic principle of Pigou, this method started to attend into political aspect in order to resolute the congestion problem in big cities.

Pigou and Friedrich Hayek point out that the assumption that the government can determine the marginal social cost of a negative externality and convert that amount into a monetary value is a weakness of the Pigouvian tax.

Arthur Pigou said: "It must be confessed, however, that we seldom know enough to decide in what fields and to what extent the State, on account of [the gaps between private and public costs] could interfere with individual choice.

Friedrich Hayek would argue that this is knowledge which could not be provided as a "given" by any "method" yet discovered, due to insuperable cognitive limits.

[43] Even if a measurement of the psychological effect of some externality did exist, it would be impossible to collect that data for all individuals affected and then find the optimum output level.

The problem, James M. Buchanan pointed out, was that the analyst had to specify the conditions under which objectively measurable costs could be ascertained by economic and policy actors.

In other words, Buchanan (like Ronald Coase) pointed out that Pigouvian tax remedies are either possible and redundant or impossible to set because the conditions presupposed for their establishment either eliminate their necessity or (if absent) preclude their enactment."

Likely instances of such include organizations intending to lower the polluter's market value as part of a pending plan to buy out its parent entity.

For one, it makes sense to impose a tax on the industry that creates the pollution problem, on the activity that emits the harmful chemicals.

It is unclear whether the harm from chlorofluorocarbons increases every year and in the same increment, or whether $1.37 per pound accurately reflects the marginal social cost of pollution.