Average cost

Average cost is an important factor in determining how businesses will choose to price their products.

For example: for a factory designed to produce a specific quantity of widgets per period—below a certain production level, average cost is higher due to under-used equipment, and above that level, production bottlenecks increase average cost.

The behavioral assumption is that the firm will choose that combination of inputs that produce the desired quantity at the lowest possible cost.

If the firm is a perfect competitor in all input markets, and thus the per-unit prices of all its inputs are unaffected by how much of the inputs the firm purchases, then it can be shown[1][2][3] that at a particular level of output, the firm has economies of scale (i.e., is operating in a downward sloping region of the long-run average cost curve) if and only if it has increasing returns to scale, the latter being exclusively a feature of the production function.

With perfect competition in the output market the long-run market equilibrium will involve all firms operating at the minimum point of their long-run average cost curves (i.e., at the borderline between economies and diseconomies of scale).

In some industries, long-run average cost is always declining (economies of scale exist indefinitely).

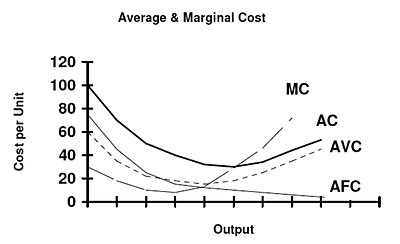

The Average Fixed Cost curve (AFC) starts from a height and goes on declining continuously as production increases.