Currency crisis

Financial institutions and the government will struggle to meet debt obligations and economic crisis may ensue.

Kaminsky et al. (1998), for instance, define currency crises as when a weighted average of monthly percentage depreciations in the exchange rate and monthly percentage declines in exchange reserves exceeds its mean by more than three standard deviations.

[8] In his article,[9] Krugman argues that a sudden speculative attack on a fixed exchange rate, even though it appears to be an irrational change in expectations, can result from rational behavior by investors.

[10] In these models, doubts about whether the government is willing to maintain its exchange rate peg lead to multiple equilibria, suggesting that self-fulfilling prophecies may be possible.

Specifically, investors expect a contingent commitment by the government and if things get bad enough, the peg is not maintained.

For example, in the 1992 ERM crisis, the UK was experiencing an economic downturn just as Germany was booming due to the reunification.

To maintain the peg to Germany, it would have been necessary for the Bank of England to slow the UK economy further by increasing its interest rates as well.

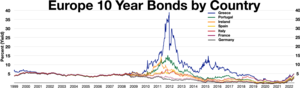

[17] According to this view, a capital flow bonanza of private funds took place during the boom years preceding this crisis into countries of Southern Europe or of the periphery of the Eurozone, including Spain, Ireland and Greece; this massive flow financed huge excesses of spending over income, i.e. bubbles, in the private sector, the public sector, or both.

[18] Others, like some of the followers of the Modern Monetary Theory (MMT) school, have argued that a region with its own currency cannot have a balance-of-payments crisis because there exists a mechanism, the TARGET system, that ensures that Eurozone member countries can always fund their current account deficits.

[19][20] These authors do not claim that the current account imbalances in the Eurozone are irrelevant but simply that a currency union cannot have a balance of payments crisis proper.