Post–World War II economic expansion

[1] The United States, the Soviet Union, Australia and Western European and East Asian countries in particular experienced unusually high and sustained growth, together with full employment.

Even countries that were relatively unaffected by the war such as Sweden (Record years) experienced considerable economic growth.

In 2000, economist Roger Middleton wrote that economic historians generally agree that 1950 represented the beginning year of the golden age,[3] while Robert Skidelsky states 1951 is the most recognized start date.

Wholesale and retail trade benefited from new highway systems, distribution warehouses, and material handling equipment such as forklifts and intermodal containers.

It was believed that large cities would be targets in a possible war, hence the highways were designed to facilitate their evacuation and ease military maneuvers.

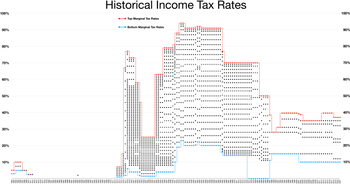

The Economist, a British publication, opposed capital levies, but supported "direct taxation heavy enough to amount to rationing of citizens' incomes"; similarly, the American economist Oliver Mitchell Wentworth Sprague, in the Economic Journal, argued that that "conscription of men should logically and equitably be accompanied by something in the nature of conscription of current income above that which is absolutely necessary".

High marginal tax rates for the wealthiest 1% were in place throughout Japan's decades of post-war growth[16] South Korea, after the Korean War saw a similar trajectory.

Structurally, the victorious Allies established the United Nations and the Bretton Woods monetary system, international institutions designed to promote stability.

In its first 7 years the CEA made five technical advances in policy making:[19] The economies of the United States, Japan, West Germany, France, and Italy did particularly well.

Japan and West Germany caught up to and exceeded the GDP of the United Kingdom during these years, even as the UK itself was experiencing the greatest absolute prosperity in its history.

Between 1947 and 1973, France went through a boom period (5% growth per year on average) dubbed by Jean Fourastié Trente Glorieuses – the title of a book published in 1979.

This rapid and sustained growth was due to the ambitions of several[quantify] Italian businesspeople, the opening of new industries (helped by the discovery of hydrocarbons, made for iron and steel, in the Po valley), re-construction and the modernisation of most Italian cities, such as Milan, Rome and Turin, and the aid given to the country after World War II (notably through the Marshall Plan).

[22][page needed][23] After 1950 Japan's economy recovered from the war damage and began to boom, with the fastest growth rates in the world.

[24] Given a boost by the Korean War, in which it acted as a major supplier to the UN force, Japan's economy embarked on a prolonged period of extremely rapid growth, led by the manufacturing sectors.

[25] In early 1950s, the Soviet Union, having reconstructed the ruins left by the war, experienced a decade of prosperous, undisturbed, and rapid economic growth, with significant and remarkable technological achievements most notably the first earth satellite.

However, the growth slowed by the mid-1960s, as the government started pouring resources into large military and space projects, and the civilian sector gradually languished.

[26] Following Khrushchev's ouster, and the appointment of a collective leadership led by Leonid Brezhnev and Alexei Kosygin, the economy was revitalised.

Sweden emerged almost unharmed from World War II, and experienced tremendous economic growth until the early 1970s, as Social Democratic Prime Minister Tage Erlander held his office from 1946 to 1969.

A 1957 speech by UK Prime Minister Harold Macmillan[29] captures what the golden age felt like, even before the brightest years which were to come in the 1960s.

Go round the country, go to the industrial towns, go to the farms and you will see a state of prosperity such as we have never had in my lifetime – nor indeed in the history of this country.Unemployment figures[30] show that unemployment was significantly lower during the Golden Age than before or after: In addition to superior economic performance, other social indexes were higher in the golden age; for example the proportion of Britain's population saying they were "very happy" fell from 52% in 1957 to just 36% in 2005.

Labor unions' support of the new policies, postponed wage increases, minimized strikes, supported technological modernization, and a policy of co-determination (Mitbestimmung), which involved a satisfactory grievance resolution system and required the representation of workers on the boards of large corporations,[36] all contributed to such a prolonged economic growth.

The recovery was accelerated by the currency reform of June 1948, US gifts of $1.4 billion Marshall Plan aid, the breaking down of old trade barriers and traditional practices, and the opening of the global market.

In the United States, the middle-class began a mass migration away from the cities and towards the suburbs; it was a period of prosperity in which most people could enjoy a job for life, a house, and a family.

In the West, there emerged a near-complete consensus against strong ideology and a belief that technocratic and scientific solutions could be found to most of humanity's problems, a view advanced by US President John F. Kennedy in 1962.

This optimism was symbolized through such events as the 1964 New York World's Fair, and Lyndon B. Johnson's Great Society programs, which aimed at eliminating poverty in the United States.