Central Bank of Ireland

Economist Patrick Honohan evaluates the success of the movement from a currency board to the central bank as follows: 'in contrast to many other post-colonial cases, (the currency board's) demise was not followed by a rapid depreciation and slide into semi-permanent high inflation and lack of convertibility.

In 1972 however, the Bretton Woods system of fixed exchange rates broke down, and in the wake of the 1973 oil crisis inflation in Britain increased dramatically, and economic theory would suggest that a smaller economy whose currency is pegged to a larger one will suffer the larger economy's inflation rate.

In the mid to late 1970s, opinion within the bank was moving toward breaking the link with the Pound Sterling and devaluing the Irish currency in order to limit inflationary effects from abroad.

At the following Council meeting in Bremen, Germany in June 1978 the basic features of the European Monetary System were outlined, including the creation of the ECU – European Currency Unit, a basket of the Community's currencies used to determine exchange rates, and the forerunner of the Euro.

It had been expected that the Irish Pound would appreciate in value against the Pound Sterling, and hence reduce inflation in Ireland, but in practice, Sterling appreciated considerably in value thanks to its status as a petrocurrency and to the tight monetary policies of the new British government of Margaret Thatcher.

Minutes of a meeting with the OECD indicated that while the Central Bank agreed that Irish property was overvalued it was fearful of precipitating a crash by "putting a number on it".

[11] The management ignored warnings from its own financial stability unit, according to one former staff member, whose evidence to the parliamentary inquiry was questioned by a number of other staff members,[12] and from the Economic and Social Research Institute about the scale of bank loans to property speculators and developers[13] leading to key information being suppressed.

It was reported that it sought to gag a prominent economist from talking about the fragile state of the nation's banks in relation the Irish branch of Northern Rock.

[14] The Central Bank "watered down" economic warnings about the property bubble in the run-up to the crash, blocked internal communication reaching board level due to the political interests, and "rigorously" concealed data from the relevant external supervisors on the large exposures of Irish banks to individual developers.

[15][16] In November 2007, they stated: "The Irish banking system continues to be well-placed to withstand adverse economic and sectoral developments in the short to medium term.

The underlying fundamentals of the residential market continue to appear strong and the current trend in monthly price developments does not imply a sharp correction.

"[17] After the bubble burst, Irish banks faced mounting losses which exposed them to a collapse of confidence following the Lehman Brothers bankruptcy in September 2008; they then suffered acute liquidity pressures which had to be met by Central Bank support, including emergency lending.

[23] The European Commission in a November 2010 review of the financial crisis said: "Some national supervisory authorities failed dramatically.

"[25] In 2003 a new separate division of the Central Bank, with its own chairman, chief executive, and board, was established as the Irish Financial Services Regulatory Authority.

This division of the Bank authorised and regulated all financial institutions (including insurance undertakings, collective investment funds and credit unions) in Ireland.

[28] The operations of the Financial Regulator were severely criticised in a report marked "strictly confidential and not for publication", as being poor value for money.

[32] Former Taoiseach Bertie Ahern, said that his decision in 2001 to create a new financial regulator was one of the main reasons for the collapse of the Irish banking sector and "if I had a chance again I wouldn't do it".

A July 2009 editorial in the Sunday Business Post said "returning the key powers of regulation to the Central Bank will be useless unless there is a fundamental change in the culture of the organisation.

[41] Subsequent to the parliamentary inquiry into the domestic banking crisis the organization said that the actions taken by the Central Bank combined with legislative reform and an overhaul of international regulation have enabled the organization to deliver effective supervision and financial stability measures since the crisis.

Many of the issues identified by the Inquiry relating to the Central Bank have been substantially addressed or continue to be addressed through measures including significant institutional reform, additional powers, the promotion of a culture of challenge and the implementation of the model of assertive risk-based supervision underpinned by a credible threat of enforcement.

[53] As seen in the Irish banking crisis, when global markets are stressed, several of these issues can occur simultaneously (i.e. they are not independent risks), to amplify the seriousness of the situation.

[54][55] Post the 2011–bailout, the Irish State has a debt-to-GNI* ratio of over 100%,[56][57] and will not be able to withstand such a material failing by the Central Bank of Ireland again.

[62] The Irish Celtic Tiger era was typified by large, interest-only mortgages, at high levels of loan-to-income values.

[71] In February 2018, the Central Bank expanded the little-used L–QIAIF vehicle to give the tax benefits as Section 110 SPVs but without requiring public accounts for the Irish CRO, which was how the abuses above were uncovered.

[72] In June 2018, the Central Bank reported that distressed debt funds switched €55 billion, or 25% of Irish GNI*, out of Section 110 SPVs, and presumably into L–QIAIFs.

[83][84] This was shown dramatically in July 2016 during "leprechaun economics" affair when Apple re-structured its Double Irish BEPS tool, as agreed under an ongoing EU tax-investigation into Apple in Ireland, into a new Irish CAIA arrangement BEPS tool.

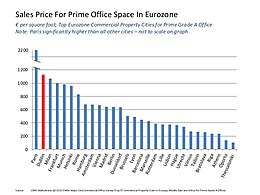

And on current trends [because Irish GDP is distorting EU–28 aggregate data], the eurozone taken as a whole may need to consider something similar.The issues post-leprechaun economics, and "Modified GNI", are captured on page 34 of the OECD 2018 Ireland survey:[88] Ireland's status as a "major tax haven", and its exposure to a handful of major U.S. multinationals, mean that its commercial property market is prone to overinflating.

[95] While the Central Bank agreed with the ESRB in 2014, it changed its mind in 2018, and decided to materially expand the L–QIAIFs vehicle (see § Light-touch regulation).

[96] Irish § Distorted economic data and the tendency to commercial and residential property bubbles has led to periods when Ireland's economy was over-leveraged and reliant on foreign capital.

[102][103][104] It is still common to see other State bodies (e.g. NTMA and IDA Ireland) present the distorted, and misleading, Debt-to-GDP data in their reports.

Brad Setser & Cole Frank

(Council on Foreign Relations) [ 77 ]