Hedge (finance)

Public futures markets were established in the 19th century[2] to allow transparent, standardized, and efficient hedging of agricultural commodity prices; they have since expanded to include futures contracts for hedging the values of energy, precious metals, foreign currency, and interest rate fluctuations.

This follows from a geometric structure formed by probabilistic representations of market views and risk scenarios.

The market values of wheat and other crops fluctuate constantly as supply and demand for them vary, with occasional large moves in either direction.

If the actual price of wheat rises greatly between planting and harvest, the farmer stands to make a lot of unexpected money, but if the actual price drops by harvest time, he is going to lose the invested money.

Therefore, the farmer has reduced his risks to fluctuations in the market of wheat because he has already guaranteed a certain number of bushels for a certain price.

The exchanges and clearing houses allow the buyer or seller to leave the contract early and cash out.

But the hedge – the short sale of Company B – nets a profit of $25 during a dramatic market collapse.

An efficient way to lower the ESO risk is to sell exchange traded calls and, to a lesser degree,[clarification needed] to buy puts.

A New England Patriots fan, for example, could bet their opponents to win to reduce the negative emotions felt if the team loses a game.

To hedge against a long futures trade a short position in synthetics can be established, and vice versa.

Stack hedging is a strategy which involves buying various futures contracts that are concentrated in nearby delivery months to increase the liquidity position.

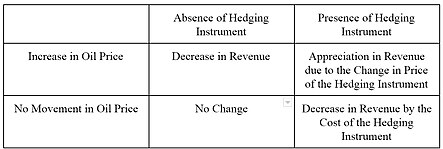

However, the party who pays the difference is "out of the money" because without the hedge they would have received the benefit of the pool price.

As investors became more sophisticated, along with the mathematical tools used to calculate values (known as models), the types of hedges have increased greatly.

As the term hedging indicates, this risk mitigation is usually done by using financial instruments, but a hedging strategy as used by commodity traders like large energy companies, is usually referring to a business model (including both financial and physical deals).

In order to show the difference between these strategies, consider the fictional company BlackIsGreen Ltd trading coal by buying this commodity at the wholesale market and selling it to households mostly in winter.

Back-to-back (B2B) is a strategy where any open position is immediately closed, e.g. by buying the respective commodity on the spot market.

[8] If BlackIsGreen decides to have a B2B-strategy, they would buy the exact amount of coal at the very moment when the household customer comes into their shop and signs the contract.

Tracker hedging is a pre-purchase approach, where the open position is decreased the closer the maturity date comes.

If BlackIsGreen knows that most of the consumers demand coal in winter to heat their house, a strategy driven by a tracker would now mean that BlackIsGreen buys e.g. half of the expected coal volume in summer, another quarter in autumn and the remaining volume in winter.

A certain hedging corridor around the pre-defined tracker-curve is allowed and fraction of the open positions decreases as the maturity date comes closer.

Delta-hedging mitigates the financial risk of an option by hedging against price changes in its underlying.

Only if BlackIsGreen chooses to perform delta-hedging as strategy, actual financial instruments come into play for hedging (in the usual, stricter meaning).

A natural hedge is an investment that reduces the undesired risk by matching cash flows (i.e. revenues and expenses).

For example, an exporter to the United States faces a risk of changes in the value of the U.S. dollar and chooses to open a production facility in that market to match its expected sales revenue to its cost structure.